GLP-1 therapies have rapidly evolved from specialized diabetes drugs to a global cultural and economic force. Once confined to endocrinology, they now shape everyday conversations on weight management, lifestyle change, and even shifting ideals of health and beauty. Their influence extends beyond the clinic into mainstream media, consumer culture, and public debate.

Polarized Discourse

Sentiment Split

Hover or tap

Data is normalised and presented on a scale from 0–100.

Positive — 39.4%

Weight-loss success, effective treatment, and pharmaceutical innovation.

Negative — 37.2%

Side effects, costs, and ethical concerns.

Neutral — 23.4%

Questions or informational posts from new, curious consumers.

Our AI-driven analysis of social platforms (TikTok, Reddit, X/Twitter, forums) and global search signals (2021–2025) reveals a strikingly divided narrative. Roughly four in ten conversations (39.4%) highlight optimism and excitement - celebrating transformative weight loss outcomes, improved metabolic health, and renewed energy. Almost as many (37.2%) voice concerns: drug shortages, affordability challenges, side-effects like nausea and fatigue, and ethical debates over off-label or cosmetic use. The remainder (23.4%) reflects a neutral, informational layer - trial updates, dosing questions, and factual reporting that anchor public understanding.

Analysis showcases UGC (User Generated Content) across 4 web sources (X, Reddit, YouTube & Google) covering content on GLP-1 as a subject & category, associated aspects, leading products and innovative approaches within the GLP-1 space.

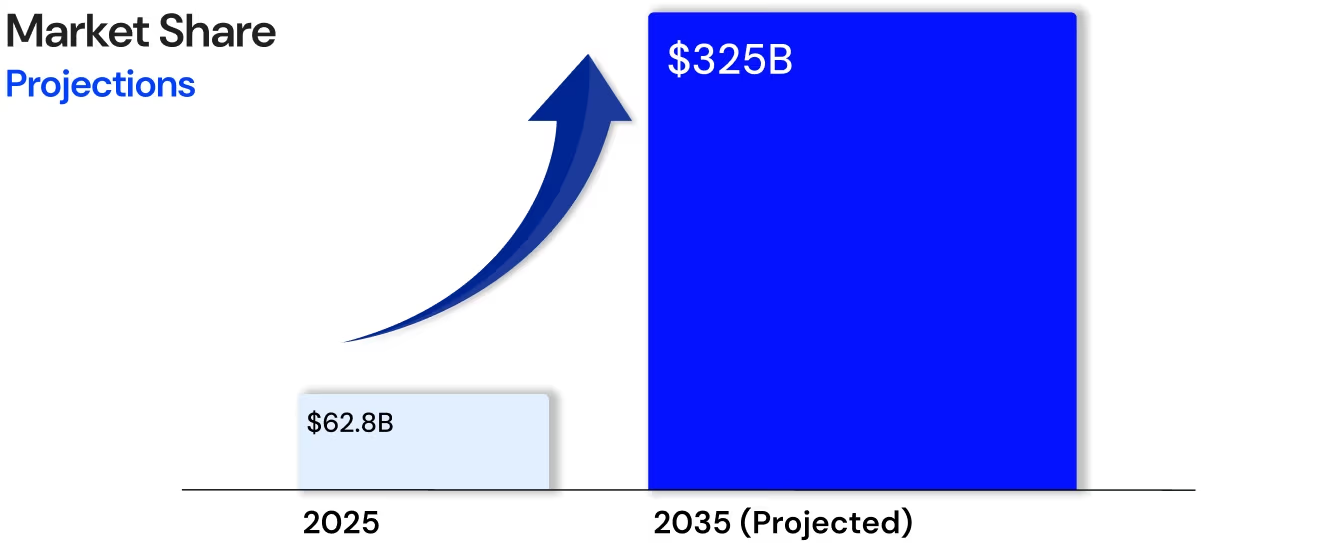

This near-equal split shows that GLP-1 adoption is driven not only by clinical data but also by public perception, digital narratives, and lived experiences. In 2025, the GLP-1 market already exceeds $62.8 billion, with projections as high as $325 billion by 2035. Yet cultural excitement and consumer anxiety remain tightly interwoven. How stakeholders respond- addressing cost, safety, and expectation management- will determine whether GLP-1s remain a breakthrough therapy for the few or expand into a foundation of preventive medicine for the many.

Explosive Market Growth

The GLP-1 receptor agonist market has entered an unprecedented growth phase. In 2025, global revenues are estimated at $62.8 billion, up from $53.5 billion in 2024. Projections indicate expansion to between $150 billion and $325 billion by 2035, powered by broader therapeutic indications, new formulations, and wider insurance coverage.

Regional Leadership

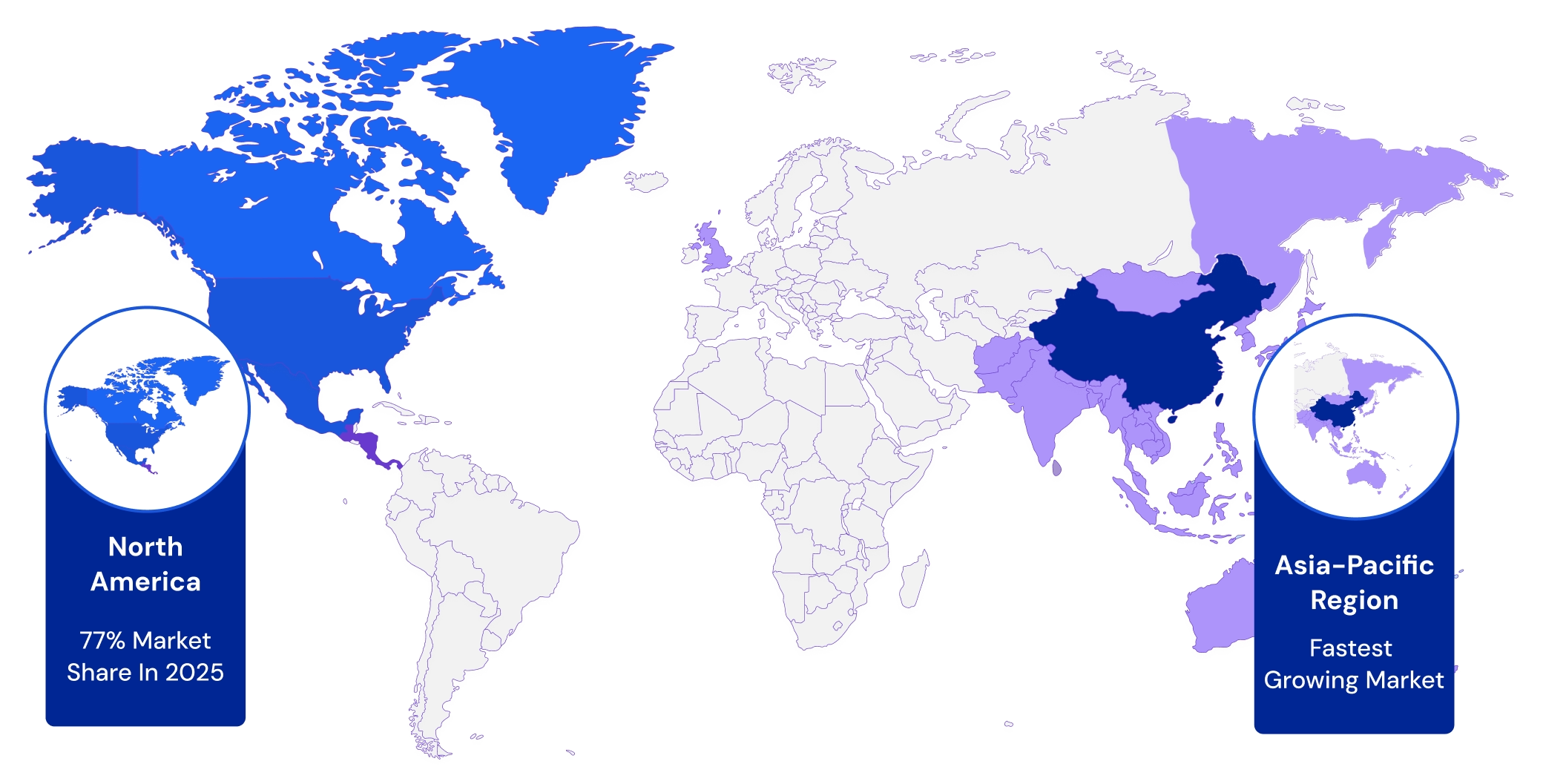

North America & Asia-Pacific Region- Market Leaders

North America dominates with an estimated 77% share of global revenues in 2025, reflecting high adoption, payer support, and robust R&D investment. The Asia-Pacific region is the fastest-growing market, driven by surging obesity and diabetes rates, improved healthcare infrastructure, and accelerating regulatory approvals. Europe contributes steadily through EMA approvals, but disparities across geographies remain stark, with low and middle-income markets showing limited access and awareness.

Prescription Trends

In the United States, GLP-1 prescriptions for obesity climbed 587% between 2019 and 2024 as adult obesity prescribing increased nearly 20-fold in the same period.

This surge is driven by new clinical efficacy data, celebrity and social media influence (notably TikTok and direct-to-consumer health platforms), increased awareness of obesity as a treatable chronic disease, and broadening guidelines from medical societies.

By 2024, GLP-1s accounted for 10.5% of all annual pharmacy claims in the US.

Demand has outpaced supply nationally, leading to shortages, expanded use of compounding pharmacies, and changing patterns in obesity-management clinic visits.

Innovation & Expansion

Globally, over 300 GLP-1-based formulations are in active clinical development, ranging from oral tablets (like orforglipron) to dual- and triple-agonist therapies aimed at improving efficacy and reducing side effects.

Innovation is particularly intense around oral GLP-1s, which offer easier administration and have prompted major pharmaceutical investment, alongside injectable and patch-based delivery mechanisms under investigation for regulatory approval.

Combination treatments targeting obesity, diabetes, cardiovascular disease, NASH, renal, hepatic, and sleep disorders are progressing through clinical trials, reflecting mainstream acceptance of GLP-1s as multi-platform therapies.

Pipeline drugs aim to overcome current side effect profiles, provide longer-lasting effects, and include consumer-friendly features- anticipated to further accelerate adoption through 2028.

Challenges

Affordability and equity issues remain formidable: surveys show 64% of potential patients cite cost as a major obstacle, with pricing averaging $1,000 per month and insurance coverage often restrictive due to prior authorization or step therapy requirements.

Insurers express growing concern as GLP-1s now comprise over one-tenth of annual pharmacy claims, prompting payer restrictions and heightened scrutiny of overall costs and coverage expansion.

Persistent supply-demand imbalances, patchy Medicaid/private insurance coverage, and price inequities across regions reinforce access gaps- especially among marginalized and lower-income populations.

Without substantial policy reforms, pricing innovation, and coverage expansion, projected growth will likely further increase access disparities and frustrate population health goals.

GLP-1 Landscape

Leading Products In The Category

2017

Ozempic®

by Novo Nordisk

💉

Injectable GLP-1

A well-known GLP-1 medication for type 2 diabetes management.

Consumer Reports

Users share successful weight loss alongside improved glycemic control, reinforcing its reliability.

Cost and access hurdles are recurring concerns for many patients.

Recent discussions highlight mental-health impacts and the need for long-term research.

2021

Wegovy®

by Novo Nordisk

💉

Injectable GLP-1

A well-known GLP-1 medication for type 2 diabetes management.

Consumer Reports

Strong weight-loss outcomes and user satisfaction are frequently mentioned.

Common side effects (e.g., nausea) are usually manageable.

Awareness campaigns continue to drive interest and engagement.

2023

Zepbound™

by Eli Lilly

💉

Injectable GLP-1

A GLP-1 receptor agonist approved for weight management and glycemic control.

Consumer Reports

Users report significant results in both weight loss and appetite suppression.

Improved blood sugar levels are widely discussed.

GI side effects are noted by early users; monitoring and support recommended.

2022

Mounjaro™

by Eli Lilly

💉

Dual GIP/GLP-1

A dual GIP and GLP-1 receptor agonist for diabetes management.

Consumer Reports

Rapid weight-loss and strong glycemic control make it a standout option.

Accessibility and affordability remain challenges for some.

Mixed experiences with side effects vs. other GLP-1s fuel ongoing debate.

2019

Rybelsus®

by Novo Nordisk

💊

Oral GLP-1

An oral GLP-1 medication for type 2 diabetes.

Consumer Reports

Oral convenience is a major plus; adherence to timing is important.

Positive trends in weight-loss and glycemic control are common.

GI side effects appear similar to injectables for some users.

2021

Semaglutide Injection

(Generic)

💉

Generic Injectable

Various generics available following the patent expiry of branded versions.

Consumer Reports

Effectiveness comparable to branded products in many reports.

Quality and regulation discussions highlight the need for assurance.

Market Leaders

How Digital Attention Varies Across Therapies

Ozempic

The undisputed category leader that consistently dominates digital search volumes and anchors the entire therapeutic space.

Consistently dominates search volumes

Anchoring the category

Established market presence

Wegovy

Gained significant momentum following regulatory approvals, with notable spikes driven by label expansions.

2021 FDA approval for obesity

Cardiovascular label expansion (2024)

Strong growth trajectory

Mounjaro

Surged after approval, leveraging innovative dual mechanism technology to capture significant market attention.

2022 approval surge

Dual GIP/GLP-1 innovation

Technology-driven growth

Zepbound

Emerged as a fast-rising contender with rapid demand acceleration following recent approvals and indication expansions.

Late 2023 approval

OSA indication in 2024

Accelerated demand growth

Rybelsus

Maintains consistent presence with unique oral delivery advantage, highlighting potential for broader market adoption.

Smaller but steady share

Oral delivery potential

Broadening adoption opportunity

Semaglutide Injection

Holds firm digital presence as a foundational GLP-1 option, recognized for broad use and wide patient familiarity.

Established reputation as an injectable GLP-1

Frequently referenced for diabetes and off-label weight management

Steady user-driven search activity, reflecting reliability and ongoing clinical relevance

Understanding Voices

GLP-1 Pharmaceutical Products Landscape

🔎

Min Share of Voice: 0%

Positive

Neutral

Negative

Sentiment Landscape

GLP-1 Conversations (2021–2025)

2021

From cautious neutrality to Wegovy’s approval spike; shortages and costs end the year on a negative note.

📰 Early 2021 — cautious outlook

Feb 2021 • Sentiment

Neutral/negative baseline; concerns: GI effects, off-label, high costs.

💊 Wegovy FDA approval

Jun 2021 • Approval

Catalyzes major positive shift; strong efficacy highlighted.

🚚 Late 2021 — shortages & costs

Nov 2021 • Access

Supply constraints, ~$1000/month cost, kidney-risk reports and GI effects drive negativity.

2022

Viral social moments drive enthusiasm but supply/access issues and lawsuits temper sentiment.

FDA halts dampen access; ~2000 GI-lawsuit references.

📈 HFpEF & market outlook

Jun 2025 • Clinical

HFpEF signals and >$300B market outlook; Ozempic dominates chatter.

Public discourse around GLP-1 therapies has been dynamic, marked by alternating waves of optimism, turbulence, and cautious stabilization. From early breakthroughs to mainstream cultural virality, the conversation illustrates how scientific milestones and media narratives can rapidly reshape sentiment.

Sentiment Journey

The Innovation Curve

Early optimismCultural turbulenceValidation → stabilization

Public perception is nearly as influential as clinical trial outcomes in shaping adoption, regulatory focus, and cultural acceptance.

Most Frequent Words

Weight management and metabolic health dominate public discourse, as evidenced by the frequency of terms like "weight," "weightloss," "obesity," "diet," "exercise," and "calorie." This underscores the centrality of GLP-1 drugs in conversations about not just diabetes control, but holistic body health, lifestyle changes, and personal transformation. The word cloud confirms GLP-1s are widely associated with broader wellness goals, not limited to disease management.

Brand awareness and product comparisons are highly prevalent, with drug names such as "ozempic," "wegovy," "mounjaro," "zepbound," "semaglutide," and "tirzepatide" appearing prominently. This signals intense consumer and patient interest in differentiating drug types, understanding new therapies, and evaluating efficacy, safety, and accessibility. It also highlights ongoing competition and the importance of pharmaceutical branding.

Barriers and challenges to access stand out, with frequent mentions of "prescription," "insurance," "pharmacy," "price," "shortage," and "compound." These words point to complex real-world issues around cost, supply availability, entry to treatment (prescription requirements), and evolving solutions like compounding, all major themes driving market dynamics and patient frustration.

Medical and clinical concerns remain top-of-mind, illustrated by recurring terms such as "side effect," "problem," "risk," "benefit," "stomach," and "nausea." These words reveal that while excitement about benefits runs high, conversations are equally focused on adverse events and real-world patient experiences, reinforcing the need for robust education and support.

Engagement with healthcare professionals and health literacy is substantial, seen in frequent references to "doctor," "patient," "control," "diabetic," "medicine," and "understand." This stresses the ongoing dialogue between patients and practitioners and the role of informed choice, medical oversight, and education in safe, effective GLP-1 adoption.

Key Drivers Of Influence

Factors Shaping Public Perception & Market Dynamics

1

Celebrity Endorsements

Elon MuskOprahChelsea Handler

Created measurable spikes in online searches

Increased media coverage significantly

Blurred lines between medical advice and lifestyle

Shaped the “miracle drug” narrative

High Influence

2

TikTok & Social Media Virality

#Ozempic#OzempicFaceBillions of views

Normalized conversations around the topic

Short-form content drives engagement

Amplifies off-label use discussions

Fuels misinformation without clinical accuracy

Mixed Impact

3

Media & Pop Culture Integration

Comedy SketchesDocumentariesMainstream Media

Entered cultural mainstream conversation

Framed as revolutionary science

Portrayed as controversial shortcuts

Reinforces both hype and skepticism

Cultural Shift

4

Digital Marketing Campaigns

RoHimsPatient Testimonials

Pharmaceutical ads magnify reach

Tele-health startups drive promotion

Saturation triggers “ad fatigue”

Aggressive tactics may undermine trust

Market Growth

5

Misinformation & Skepticism

Counterfeit IssuesSide EffectsAccess Concerns

Conversations about counterfeit injections

Exaggerated side-effects narratives

“Celebrity-only” access perception

Creates reputational risks for providers

Risk Factor

The rise of GLP-1s is not only a clinical story - it is a cultural phenomenon amplified by digital ecosystems. Traditional drug adoption curves were driven by physician detailing and clinical guidelines. In contrast, GLP-1 awareness has been shaped by this loop.

Viral Feedback Loop

Amplified By Digital Ecosystems

Circular map of influence drivers with directional links. Link thickness encodes strength; dashed links represent moderating effects.

This loop has dramatically accelerated demand, sometimes outpacing prescriber guidance and regulatory readiness. It also shows how modern therapies can be propelled into the spotlight by cultural catalysts as much as by scientific milestones.

Consumer Search Trends

GLP-1 & Top Products Within Category

Avg. Global Monthly Searches: 10.9M

Averages across GLP-1, Ozempic, Zepbound, Wegovy, Mounjaro, Rybelsus, and Semaglutide Injection.

The sustained and growing volume of global monthly searches across all six GLP-1 drugs reflects a heightened and expanding consumer curiosity and engagement worldwide. This trend indicates that GLP-1 therapies have moved beyond specialist circles into mainstream awareness, driven by increasing public discourse around obesity and diabetes management. The steady climb from around 900,000 searches weekly in early 2023 to peaks exceeding 2 million by mid-2025 underscores how demand for information mirrors heightened product adoption, regulatory approvals, and media coverage at a global scale.

The clear seasonal fluctuations observed in search patterns, with consistent peaks during spring (March-April) and fall (October-November), likely correspond to periods when consumers become more focused on health-related behavior changes, such as post-winter resolutions or pre-holiday weight management efforts. Coupled with social media trends and major marketing campaigns released cyclically, these seasonal spikes reveal important windows for targeted educational outreach and promotional activities to optimize patient awareness and engagement aligned to consumer health cycles.

The recent average search volume plateauing above 2 million monthly searches in 2025 signals a maturing but highly active market landscape where interest remains intense but competitive. This persistence in high search activity demonstrates robust market health and suggests sustained opportunities for pharmaceutical innovation, telehealth expansion, and digital marketing refinement. For stakeholders, continuing to analyze such search trends can uncover emerging consumer concerns, variations in drug preference, and regional access issues critical for strategic decision-making and patient-centric educational programming in the GLP-1 domain.

Consumer Search Trends — Leading Products

Consumer Search Trends

Leading Products

Ozempic maintains dominant consumer interest across the timeline, consistently showing the highest weekly search volumes. Its search popularity peaks above 1,060,000, reflecting sustained market leadership and strong consumer engagement driven by broad brand recognition and perceived efficacy.

Wegovy and Mounjaro show significant growth trajectories, with peak weekly searches crossing 400,000 and 630,000 respectively by early to mid-2025. These trends demonstrate their rising market presence and increasing consumer curiosity, positioning them as strong contenders challenging Ozempic’s dominance in the GLP-1 space.

Emerging competitors like Zepbound have carved a smaller but steady niche, peaking around 190,000 weekly searches and showing gradual adoption. Meanwhile, Rybelsus and Semaglutide Injection register lower search volumes indicative of niche or specialized use cases, but their consistent search presence highlights an established patient base and ongoing relevance within the category.

GLP-1 Product Development Topics

Progress On X (Twitter) Since 2023

Data is normalised and presented on a scale from 0–100, where each point on the graph is divided by the highest point, or 100.

Increasing Interest in GLP-1 Products on Social Media The GLP-1 Products category shows a steady upward trend over the period, starting around 47 in January 2023 and reaching a peak near 83 by November 2024. This signals growing public and expert engagement with specific GLP-1 drugs on Twitter, reflecting heightened consumer awareness, discussion about new launches, and ongoing real-world experiences shared around these therapies.

Fluctuating but Overall Rising Research & Development Conversations Research and Development (R&D) discussions show some month-to-month variability but maintain a solid upward momentum overall, increasing from about 40 in early 2023 to above 68 by mid-2025. This reflects sustained industry and academic focus on innovation, clinical trials, and new indications for GLP-1 drugs, underscoring active pipeline advancements and emerging therapeutic applications.

Moderate but Increasing Focus on Pharmaceutical Innovation Conversations related to Pharmaceutical Innovation began strong in the 50–70 range and experienced fluctuations yet trending upward towards 68 by mid-2025. This indicates increasing attention on manufacturing breakthroughs, novel delivery pathways, and next-generation product formulations that promise improved efficacy, safety, and patient convenience within the GLP-1 marketplace.

GLP-1 Application Topics

Progress On X (Twitter) Since 2023

Data is normalised and presented on a scale from 0–100, where each point on the graph is divided by the highest point, or 100.

Dominant Focus on Weight Loss Medications and Fluctuating Interest in Diabetes Management Throughout the period, "Weight Loss Medications" consistently hold the highest relative interest among the three application topics, starting above 54% and maintaining generally strong engagement around 50-70%. In contrast, "Diabetes Management" exhibits a downward trend from peak engagement near 83% in early 2023 to lower 30-50% levels by mid-2024, indicating a gradual shift of social media conversations towards obesity and weight loss as primary focal points within the GLP-1 discourse.

Significant Spikes in Health Risks Discussions with Increasing Frequency The "Health Risks" category shows notable variability but a marked increase in interest starting mid-2023, with peaks near 50% or higher, especially in July-August 2023 and again in early 2025. This rise likely reflects growing public and professional attention to adverse effects, safety concerns, and controversy surrounding GLP-1 drug use, highlighting the importance of addressing real-world clinical risks in ongoing education and communication efforts.

Social Media Conversations Reflect a Dynamic and Evolving Narrative Around GLP-1 Applications The interplay between the three application topics- weight loss, diabetes management, and health risks- reveals a complex, evolving landscape on social platforms. While weight loss dominates as the most discussed application, heightened health risk awareness periodically gains traction, and diabetes remains a foundational but relatively less emphasized theme over time, illustrating how user focus shifts in response to emerging data, marketing, and societal concerns on digital discourse platforms like Twitter.

Conclusion

This report delivers a comprehensive synthesis of hundreds of thousands of user-generated posts, comments, and discussions from four leading digital platforms, spanning a multi-year horizon of the GLP-1 drug landscape. By integrating quantitative search trends, evolving sentiment patterns, and platform-specific behavioral insights, the analysis illuminates not only what drives public interest, but how market leaders are shaped and scrutinized in real time.

Through the detailed examination of digital attention, emerging innovation, product-specific dynamics, and evolving public discourse, these findings offer an authentic, data-driven perspective on how the GLP-1 category is experienced by patients, healthcare professionals, and the wider public. The collective narrative underscored here demonstrates that the GLP-1 therapeutic space is both highly dynamic and polarized, shaped by waves of endorsement, criticism, breakthrough announcements, and ongoing patient and provider feedback.

As the GLP-1 segment continues to expand- with digital touchpoints playing an ever-larger role in awareness, demand, and reputation, these insights equip stakeholders across pharma, healthcare, and policy to better anticipate trends, address concerns, and inform evidence-based decision making in this rapidly evolving field.

GLP-1 Digital Landscape: Product, Sentiment & Trends Report

A multi-platform analysis capturing hundreds of thousands of real consumer and professional insights, this report uncovers how digital attention, search trends, and user sentiment shape the market leaders and innovations in GLP-1 therapies. Explore product-specific momentum, evolving topics, and data-backed perspectives on diabetes, obesity, and beyond- all distilled from the online pulse driving the GLP-1 revolution.

Innovation

Overview

The Shift

GLP-1 therapies have rapidly evolved from specialized diabetes drugs to a global cultural and economic force. Once confined to endocrinology, they now shape everyday conversations on weight management, lifestyle change, and even shifting ideals of health and beauty. Their influence extends beyond the clinic into mainstream media, consumer culture, and public debate.

Polarized Discourse

Sentiment Split

Hover or tap

Data is normalised and presented on a scale from 0–100.

Positive — 39.4%

Weight-loss success, effective treatment, and pharmaceutical innovation.

Negative — 37.2%

Side effects, costs, and ethical concerns.

Neutral — 23.4%

Questions or informational posts from new, curious consumers.

Our AI-driven analysis of social platforms (TikTok, Reddit, X/Twitter, forums) and global search signals (2021–2025) reveals a strikingly divided narrative. Roughly four in ten conversations (39.4%) highlight optimism and excitement - celebrating transformative weight loss outcomes, improved metabolic health, and renewed energy. Almost as many (37.2%) voice concerns: drug shortages, affordability challenges, side-effects like nausea and fatigue, and ethical debates over off-label or cosmetic use. The remainder (23.4%) reflects a neutral, informational layer - trial updates, dosing questions, and factual reporting that anchor public understanding.

Analysis showcases UGC (User Generated Content) across 4 web sources (X, Reddit, YouTube & Google) covering content on GLP-1 as a subject & category, associated aspects, leading products and innovative approaches within the GLP-1 space.

This near-equal split shows that GLP-1 adoption is driven not only by clinical data but also by public perception, digital narratives, and lived experiences. In 2025, the GLP-1 market already exceeds $62.8 billion, with projections as high as $325 billion by 2035. Yet cultural excitement and consumer anxiety remain tightly interwoven. How stakeholders respond- addressing cost, safety, and expectation management- will determine whether GLP-1s remain a breakthrough therapy for the few or expand into a foundation of preventive medicine for the many.

Explosive Market Growth

The GLP-1 receptor agonist market has entered an unprecedented growth phase. In 2025, global revenues are estimated at $62.8 billion, up from $53.5 billion in 2024. Projections indicate expansion to between $150 billion and $325 billion by 2035, powered by broader therapeutic indications, new formulations, and wider insurance coverage.

Regional Leadership

North America & Asia-Pacific Region- Market Leaders

North America dominates with an estimated 77% share of global revenues in 2025, reflecting high adoption, payer support, and robust R&D investment. The Asia-Pacific region is the fastest-growing market, driven by surging obesity and diabetes rates, improved healthcare infrastructure, and accelerating regulatory approvals. Europe contributes steadily through EMA approvals, but disparities across geographies remain stark, with low and middle-income markets showing limited access and awareness.

Prescription Trends

In the United States, GLP-1 prescriptions for obesity climbed 587% between 2019 and 2024 as adult obesity prescribing increased nearly 20-fold in the same period.

This surge is driven by new clinical efficacy data, celebrity and social media influence (notably TikTok and direct-to-consumer health platforms), increased awareness of obesity as a treatable chronic disease, and broadening guidelines from medical societies.

By 2024, GLP-1s accounted for 10.5% of all annual pharmacy claims in the US.

Demand has outpaced supply nationally, leading to shortages, expanded use of compounding pharmacies, and changing patterns in obesity-management clinic visits.

Innovation & Expansion

Globally, over 300 GLP-1-based formulations are in active clinical development, ranging from oral tablets (like orforglipron) to dual- and triple-agonist therapies aimed at improving efficacy and reducing side effects.

Innovation is particularly intense around oral GLP-1s, which offer easier administration and have prompted major pharmaceutical investment, alongside injectable and patch-based delivery mechanisms under investigation for regulatory approval.

Combination treatments targeting obesity, diabetes, cardiovascular disease, NASH, renal, hepatic, and sleep disorders are progressing through clinical trials, reflecting mainstream acceptance of GLP-1s as multi-platform therapies.

Pipeline drugs aim to overcome current side effect profiles, provide longer-lasting effects, and include consumer-friendly features- anticipated to further accelerate adoption through 2028.

Challenges

Affordability and equity issues remain formidable: surveys show 64% of potential patients cite cost as a major obstacle, with pricing averaging $1,000 per month and insurance coverage often restrictive due to prior authorization or step therapy requirements.

Insurers express growing concern as GLP-1s now comprise over one-tenth of annual pharmacy claims, prompting payer restrictions and heightened scrutiny of overall costs and coverage expansion.

Persistent supply-demand imbalances, patchy Medicaid/private insurance coverage, and price inequities across regions reinforce access gaps- especially among marginalized and lower-income populations.

Without substantial policy reforms, pricing innovation, and coverage expansion, projected growth will likely further increase access disparities and frustrate population health goals.

GLP-1 Landscape

Leading Products In The Category

2017

Ozempic®

by Novo Nordisk

💉

Injectable GLP-1

A well-known GLP-1 medication for type 2 diabetes management.

Consumer Reports

Users share successful weight loss alongside improved glycemic control, reinforcing its reliability.

Cost and access hurdles are recurring concerns for many patients.

Recent discussions highlight mental-health impacts and the need for long-term research.

2021

Wegovy®

by Novo Nordisk

💉

Injectable GLP-1

A well-known GLP-1 medication for type 2 diabetes management.

Consumer Reports

Strong weight-loss outcomes and user satisfaction are frequently mentioned.

Common side effects (e.g., nausea) are usually manageable.

Awareness campaigns continue to drive interest and engagement.

2023

Zepbound™

by Eli Lilly

💉

Injectable GLP-1

A GLP-1 receptor agonist approved for weight management and glycemic control.

Consumer Reports

Users report significant results in both weight loss and appetite suppression.

Improved blood sugar levels are widely discussed.

GI side effects are noted by early users; monitoring and support recommended.

2022

Mounjaro™

by Eli Lilly

💉

Dual GIP/GLP-1

A dual GIP and GLP-1 receptor agonist for diabetes management.

Consumer Reports

Rapid weight-loss and strong glycemic control make it a standout option.

Accessibility and affordability remain challenges for some.

Mixed experiences with side effects vs. other GLP-1s fuel ongoing debate.

2019

Rybelsus®

by Novo Nordisk

💊

Oral GLP-1

An oral GLP-1 medication for type 2 diabetes.

Consumer Reports

Oral convenience is a major plus; adherence to timing is important.

Positive trends in weight-loss and glycemic control are common.

GI side effects appear similar to injectables for some users.

2021

Semaglutide Injection

(Generic)

💉

Generic Injectable

Various generics available following the patent expiry of branded versions.

Consumer Reports

Effectiveness comparable to branded products in many reports.

Quality and regulation discussions highlight the need for assurance.

Market Leaders

How Digital Attention Varies Across Therapies

Ozempic

The undisputed category leader that consistently dominates digital search volumes and anchors the entire therapeutic space.

Consistently dominates search volumes

Anchoring the category

Established market presence

Wegovy

Gained significant momentum following regulatory approvals, with notable spikes driven by label expansions.

2021 FDA approval for obesity

Cardiovascular label expansion (2024)

Strong growth trajectory

Mounjaro

Surged after approval, leveraging innovative dual mechanism technology to capture significant market attention.

2022 approval surge

Dual GIP/GLP-1 innovation

Technology-driven growth

Zepbound

Emerged as a fast-rising contender with rapid demand acceleration following recent approvals and indication expansions.

Late 2023 approval

OSA indication in 2024

Accelerated demand growth

Rybelsus

Maintains consistent presence with unique oral delivery advantage, highlighting potential for broader market adoption.

Smaller but steady share

Oral delivery potential

Broadening adoption opportunity

Semaglutide Injection

Holds firm digital presence as a foundational GLP-1 option, recognized for broad use and wide patient familiarity.

Established reputation as an injectable GLP-1

Frequently referenced for diabetes and off-label weight management

Steady user-driven search activity, reflecting reliability and ongoing clinical relevance

Understanding Voices

GLP-1 Pharmaceutical Products Landscape

🔎

Min Share of Voice: 0%

Positive

Neutral

Negative

Sentiment Landscape

GLP-1 Conversations (2021–2025)

2021

From cautious neutrality to Wegovy’s approval spike; shortages and costs end the year on a negative note.

📰 Early 2021 — cautious outlook

Feb 2021 • Sentiment

Neutral/negative baseline; concerns: GI effects, off-label, high costs.

💊 Wegovy FDA approval

Jun 2021 • Approval

Catalyzes major positive shift; strong efficacy highlighted.

🚚 Late 2021 — shortages & costs

Nov 2021 • Access

Supply constraints, ~$1000/month cost, kidney-risk reports and GI effects drive negativity.

2022

Viral social moments drive enthusiasm but supply/access issues and lawsuits temper sentiment.

FDA halts dampen access; ~2000 GI-lawsuit references.

📈 HFpEF & market outlook

Jun 2025 • Clinical

HFpEF signals and >$300B market outlook; Ozempic dominates chatter.

Public discourse around GLP-1 therapies has been dynamic, marked by alternating waves of optimism, turbulence, and cautious stabilization. From early breakthroughs to mainstream cultural virality, the conversation illustrates how scientific milestones and media narratives can rapidly reshape sentiment.

Sentiment Journey

The Innovation Curve

Early optimismCultural turbulenceValidation → stabilization

Public perception is nearly as influential as clinical trial outcomes in shaping adoption, regulatory focus, and cultural acceptance.

Most Frequent Words

Weight management and metabolic health dominate public discourse, as evidenced by the frequency of terms like "weight," "weightloss," "obesity," "diet," "exercise," and "calorie." This underscores the centrality of GLP-1 drugs in conversations about not just diabetes control, but holistic body health, lifestyle changes, and personal transformation. The word cloud confirms GLP-1s are widely associated with broader wellness goals, not limited to disease management.

Brand awareness and product comparisons are highly prevalent, with drug names such as "ozempic," "wegovy," "mounjaro," "zepbound," "semaglutide," and "tirzepatide" appearing prominently. This signals intense consumer and patient interest in differentiating drug types, understanding new therapies, and evaluating efficacy, safety, and accessibility. It also highlights ongoing competition and the importance of pharmaceutical branding.

Barriers and challenges to access stand out, with frequent mentions of "prescription," "insurance," "pharmacy," "price," "shortage," and "compound." These words point to complex real-world issues around cost, supply availability, entry to treatment (prescription requirements), and evolving solutions like compounding, all major themes driving market dynamics and patient frustration.

Medical and clinical concerns remain top-of-mind, illustrated by recurring terms such as "side effect," "problem," "risk," "benefit," "stomach," and "nausea." These words reveal that while excitement about benefits runs high, conversations are equally focused on adverse events and real-world patient experiences, reinforcing the need for robust education and support.

Engagement with healthcare professionals and health literacy is substantial, seen in frequent references to "doctor," "patient," "control," "diabetic," "medicine," and "understand." This stresses the ongoing dialogue between patients and practitioners and the role of informed choice, medical oversight, and education in safe, effective GLP-1 adoption.

Key Drivers Of Influence

Factors Shaping Public Perception & Market Dynamics

1

Celebrity Endorsements

Elon MuskOprahChelsea Handler

Created measurable spikes in online searches

Increased media coverage significantly

Blurred lines between medical advice and lifestyle

Shaped the “miracle drug” narrative

High Influence

2

TikTok & Social Media Virality

#Ozempic#OzempicFaceBillions of views

Normalized conversations around the topic

Short-form content drives engagement

Amplifies off-label use discussions

Fuels misinformation without clinical accuracy

Mixed Impact

3

Media & Pop Culture Integration

Comedy SketchesDocumentariesMainstream Media

Entered cultural mainstream conversation

Framed as revolutionary science

Portrayed as controversial shortcuts

Reinforces both hype and skepticism

Cultural Shift

4

Digital Marketing Campaigns

RoHimsPatient Testimonials

Pharmaceutical ads magnify reach

Tele-health startups drive promotion

Saturation triggers “ad fatigue”

Aggressive tactics may undermine trust

Market Growth

5

Misinformation & Skepticism

Counterfeit IssuesSide EffectsAccess Concerns

Conversations about counterfeit injections

Exaggerated side-effects narratives

“Celebrity-only” access perception

Creates reputational risks for providers

Risk Factor

The rise of GLP-1s is not only a clinical story - it is a cultural phenomenon amplified by digital ecosystems. Traditional drug adoption curves were driven by physician detailing and clinical guidelines. In contrast, GLP-1 awareness has been shaped by this loop.

Viral Feedback Loop

Amplified By Digital Ecosystems

Circular map of influence drivers with directional links. Link thickness encodes strength; dashed links represent moderating effects.

This loop has dramatically accelerated demand, sometimes outpacing prescriber guidance and regulatory readiness. It also shows how modern therapies can be propelled into the spotlight by cultural catalysts as much as by scientific milestones.

Consumer Search Trends

GLP-1 & Top Products Within Category

Avg. Global Monthly Searches: 10.9M

Averages across GLP-1, Ozempic, Zepbound, Wegovy, Mounjaro, Rybelsus, and Semaglutide Injection.

The sustained and growing volume of global monthly searches across all six GLP-1 drugs reflects a heightened and expanding consumer curiosity and engagement worldwide. This trend indicates that GLP-1 therapies have moved beyond specialist circles into mainstream awareness, driven by increasing public discourse around obesity and diabetes management. The steady climb from around 900,000 searches weekly in early 2023 to peaks exceeding 2 million by mid-2025 underscores how demand for information mirrors heightened product adoption, regulatory approvals, and media coverage at a global scale.

The clear seasonal fluctuations observed in search patterns, with consistent peaks during spring (March-April) and fall (October-November), likely correspond to periods when consumers become more focused on health-related behavior changes, such as post-winter resolutions or pre-holiday weight management efforts. Coupled with social media trends and major marketing campaigns released cyclically, these seasonal spikes reveal important windows for targeted educational outreach and promotional activities to optimize patient awareness and engagement aligned to consumer health cycles.

The recent average search volume plateauing above 2 million monthly searches in 2025 signals a maturing but highly active market landscape where interest remains intense but competitive. This persistence in high search activity demonstrates robust market health and suggests sustained opportunities for pharmaceutical innovation, telehealth expansion, and digital marketing refinement. For stakeholders, continuing to analyze such search trends can uncover emerging consumer concerns, variations in drug preference, and regional access issues critical for strategic decision-making and patient-centric educational programming in the GLP-1 domain.

Consumer Search Trends — Leading Products

Consumer Search Trends

Leading Products

Ozempic maintains dominant consumer interest across the timeline, consistently showing the highest weekly search volumes. Its search popularity peaks above 1,060,000, reflecting sustained market leadership and strong consumer engagement driven by broad brand recognition and perceived efficacy.

Wegovy and Mounjaro show significant growth trajectories, with peak weekly searches crossing 400,000 and 630,000 respectively by early to mid-2025. These trends demonstrate their rising market presence and increasing consumer curiosity, positioning them as strong contenders challenging Ozempic’s dominance in the GLP-1 space.

Emerging competitors like Zepbound have carved a smaller but steady niche, peaking around 190,000 weekly searches and showing gradual adoption. Meanwhile, Rybelsus and Semaglutide Injection register lower search volumes indicative of niche or specialized use cases, but their consistent search presence highlights an established patient base and ongoing relevance within the category.

GLP-1 Product Development Topics

Progress On X (Twitter) Since 2023

Data is normalised and presented on a scale from 0–100, where each point on the graph is divided by the highest point, or 100.

Increasing Interest in GLP-1 Products on Social Media The GLP-1 Products category shows a steady upward trend over the period, starting around 47 in January 2023 and reaching a peak near 83 by November 2024. This signals growing public and expert engagement with specific GLP-1 drugs on Twitter, reflecting heightened consumer awareness, discussion about new launches, and ongoing real-world experiences shared around these therapies.

Fluctuating but Overall Rising Research & Development Conversations Research and Development (R&D) discussions show some month-to-month variability but maintain a solid upward momentum overall, increasing from about 40 in early 2023 to above 68 by mid-2025. This reflects sustained industry and academic focus on innovation, clinical trials, and new indications for GLP-1 drugs, underscoring active pipeline advancements and emerging therapeutic applications.

Moderate but Increasing Focus on Pharmaceutical Innovation Conversations related to Pharmaceutical Innovation began strong in the 50–70 range and experienced fluctuations yet trending upward towards 68 by mid-2025. This indicates increasing attention on manufacturing breakthroughs, novel delivery pathways, and next-generation product formulations that promise improved efficacy, safety, and patient convenience within the GLP-1 marketplace.

GLP-1 Application Topics

Progress On X (Twitter) Since 2023

Data is normalised and presented on a scale from 0–100, where each point on the graph is divided by the highest point, or 100.

Dominant Focus on Weight Loss Medications and Fluctuating Interest in Diabetes Management Throughout the period, "Weight Loss Medications" consistently hold the highest relative interest among the three application topics, starting above 54% and maintaining generally strong engagement around 50-70%. In contrast, "Diabetes Management" exhibits a downward trend from peak engagement near 83% in early 2023 to lower 30-50% levels by mid-2024, indicating a gradual shift of social media conversations towards obesity and weight loss as primary focal points within the GLP-1 discourse.

Significant Spikes in Health Risks Discussions with Increasing Frequency The "Health Risks" category shows notable variability but a marked increase in interest starting mid-2023, with peaks near 50% or higher, especially in July-August 2023 and again in early 2025. This rise likely reflects growing public and professional attention to adverse effects, safety concerns, and controversy surrounding GLP-1 drug use, highlighting the importance of addressing real-world clinical risks in ongoing education and communication efforts.

Social Media Conversations Reflect a Dynamic and Evolving Narrative Around GLP-1 Applications The interplay between the three application topics- weight loss, diabetes management, and health risks- reveals a complex, evolving landscape on social platforms. While weight loss dominates as the most discussed application, heightened health risk awareness periodically gains traction, and diabetes remains a foundational but relatively less emphasized theme over time, illustrating how user focus shifts in response to emerging data, marketing, and societal concerns on digital discourse platforms like Twitter.

Conclusion

This report delivers a comprehensive synthesis of hundreds of thousands of user-generated posts, comments, and discussions from four leading digital platforms, spanning a multi-year horizon of the GLP-1 drug landscape. By integrating quantitative search trends, evolving sentiment patterns, and platform-specific behavioral insights, the analysis illuminates not only what drives public interest, but how market leaders are shaped and scrutinized in real time.

Through the detailed examination of digital attention, emerging innovation, product-specific dynamics, and evolving public discourse, these findings offer an authentic, data-driven perspective on how the GLP-1 category is experienced by patients, healthcare professionals, and the wider public. The collective narrative underscored here demonstrates that the GLP-1 therapeutic space is both highly dynamic and polarized, shaped by waves of endorsement, criticism, breakthrough announcements, and ongoing patient and provider feedback.

As the GLP-1 segment continues to expand- with digital touchpoints playing an ever-larger role in awareness, demand, and reputation, these insights equip stakeholders across pharma, healthcare, and policy to better anticipate trends, address concerns, and inform evidence-based decision making in this rapidly evolving field.

FAQs

What are GLP-1 drugs and what conditions do they treat?

GLP-1 drugs are a class of medications used to treat type 2 diabetes and obesity, and some are also approved for reducing cardiovascular risks. They work by mimicking incretin hormones that regulate blood sugar and appetite, often leading to improved glycemic control and weight reduction.

BioBrain's Insights Engine refers to BioBrain's combined AI, Automation & Agility capabilities which are designed to enhance the efficiency and effectiveness of market research processes through the use of sophisticated technologies. Our AI systems leverage well-developed advanced natural language processing (NLP) models and generative capabilities created as a result of broader world information. We have combined these capabilities with rigorously mapped statistical analysis methods and automation workflows developed by researchers in BioBrain’s product team. These technologies work together to drive processes, cumulatively termed as ‘Insight Engine’ by BioBrain Insights. It streamlines and optimizes market research workflows, enabling the extraction of actionable insights from complex data sets through rigorously tested, intelligent workflows.

Are there any precautions or drug interactions?

Patients should inform their doctor of all medications and conditions. GLP-1 drugs are not quick-fix solutions, misuse and unsupervised switching between drugs can raise risks. Regular follow-up is essential for managing side effects and ensuring sustained benefit.

BioBrain's Insights Engine refers to BioBrain's combined AI, Automation & Agility capabilities which are designed to enhance the efficiency and effectiveness of market research processes through the use of sophisticated technologies. Our AI systems leverage well-developed advanced natural language processing (NLP) models and generative capabilities created as a result of broader world information. We have combined these capabilities with rigorously mapped statistical analysis methods and automation workflows developed by researchers in BioBrain’s product team. These technologies work together to drive processes, cumulatively termed as ‘Insight Engine’ by BioBrain Insights. It streamlines and optimizes market research workflows, enabling the extraction of actionable insights from complex data sets through rigorously tested, intelligent workflows.

Who is eligible for GLP-1 medications?

Healthcare providers prescribe GLP-1 drugs for adults with type 2 diabetes, overweight or obesity (BMI ≥30, or ≥27 with comorbidities), or cardiovascular risks. They are not suitable for pregnant or breastfeeding individuals, those with a history of pancreatitis or thyroid cancer, or those with certain rare genetic syndromes.

BioBrain's Insights Engine refers to BioBrain's combined AI, Automation & Agility capabilities which are designed to enhance the efficiency and effectiveness of market research processes through the use of sophisticated technologies. Our AI systems leverage well-developed advanced natural language processing (NLP) models and generative capabilities created as a result of broader world information. We have combined these capabilities with rigorously mapped statistical analysis methods and automation workflows developed by researchers in BioBrain’s product team. These technologies work together to drive processes, cumulatively termed as ‘Insight Engine’ by BioBrain Insights. It streamlines and optimizes market research workflows, enabling the extraction of actionable insights from complex data sets through rigorously tested, intelligent workflows.

How do GLP-1 drugs work in the body?

GLP-1 drugs help the pancreas release more insulin after eating, slow down the rate of digestion, and signal the brain to reduce hunger, which collectively supports blood sugar management and appetite control. Some newer options also target a second hormone (GIP) for increased effectiveness.

BioBrain's Insights Engine refers to BioBrain's combined AI, Automation & Agility capabilities which are designed to enhance the efficiency and effectiveness of market research processes through the use of sophisticated technologies. Our AI systems leverage well-developed advanced natural language processing (NLP) models and generative capabilities created as a result of broader world information. We have combined these capabilities with rigorously mapped statistical analysis methods and automation workflows developed by researchers in BioBrain’s product team. These technologies work together to drive processes, cumulatively termed as ‘Insight Engine’ by BioBrain Insights. It streamlines and optimizes market research workflows, enabling the extraction of actionable insights from complex data sets through rigorously tested, intelligent workflows.

What are possible side effects or risks of GLP-1 Drugs?

Common side effects include nausea, vomiting, diarrhea, stomach pain, and headaches; most are mild and temporary. Serious risks can include pancreatitis, gallstones, kidney injury, and potential thyroid issues. Long-term safety continues to be monitored through ongoing research and real-world use.

BioBrain's Insights Engine refers to BioBrain's combined AI, Automation & Agility capabilities which are designed to enhance the efficiency and effectiveness of market research processes through the use of sophisticated technologies. Our AI systems leverage well-developed advanced natural language processing (NLP) models and generative capabilities created as a result of broader world information. We have combined these capabilities with rigorously mapped statistical analysis methods and automation workflows developed by researchers in BioBrain’s product team. These technologies work together to drive processes, cumulatively termed as ‘Insight Engine’ by BioBrain Insights. It streamlines and optimizes market research workflows, enabling the extraction of actionable insights from complex data sets through rigorously tested, intelligent workflows.

Sign up for latest market research updates.

Uncover hidden trends & industry shifts. Get the latest market research insights delivered to your inbox.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Sign up for latest market research updates.

Uncover hidden trends & industry shifts. Get the latest market research insights delivered to your inbox.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.avif)